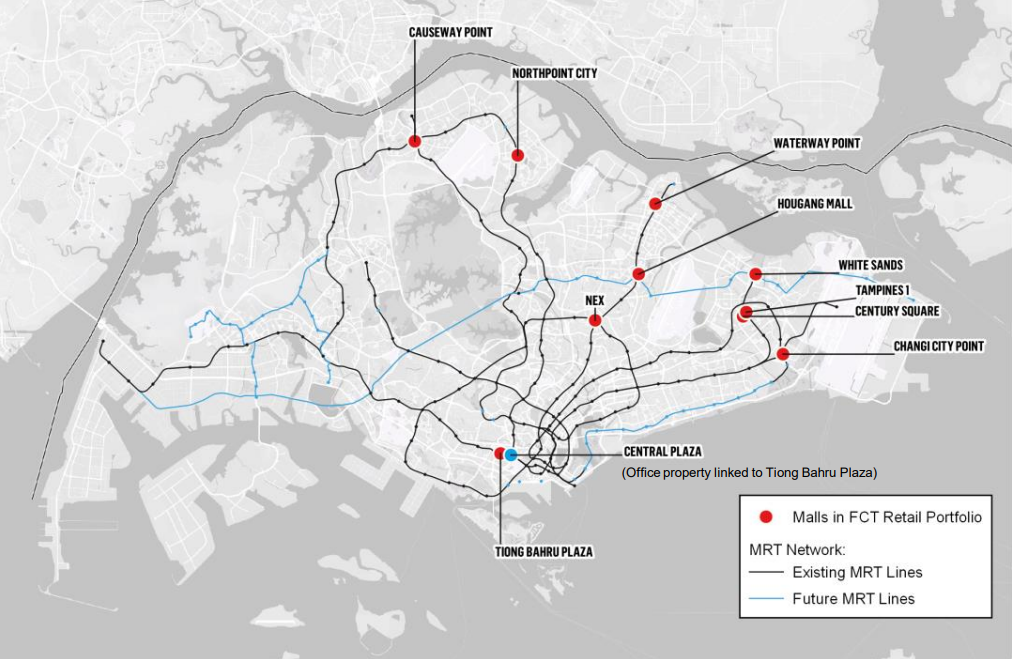

Frasers Centrepoint Trust (SGX: J69U) is Singapore’s biggest player in the suburban retail space now with 10 quality retail malls focused on providing Essential Services to mainly domestic catchment. As suburban malls were among the first to benefit from the post-pandemic recovery, investors are now thinking if Frasers Centrepoint Trust (FCT) is a good investment while we continue to ride on the recovery wave back to pre-pandemic levels. As the FY2023 results are just released, let’s take a deep dive into Frasers Centrepoint Trust’s track record, portfolio performance, and long-term growth catalysts as well as risks that investors should know about before investing.

Portfolio Overview

As of 30 September 2023, we can see that Frasers Centrepoint Trust has a very strong portfolio with well-populated and well-connected malls in Singapore’s suburban area. On top of this, they also have a significant stake (30.97%) in Hektar REIT. It is important to note that Frasers Centrepoint Trust is currently undergoing the divestment of Changi City Point as well as a majority portion of its stake in Hektar REIT, which is expected to complete on 15 November 2023 and Q4 of 2023 respectively. We will dive deeper into the divestment and its pro-forma effects later in this article.

It is always good to see a REIT’s management being so active in rejuvenating and improving the overall portfolio, not only through acquisitions but also through meaningful divestments as well. Although FCT will see slight decreases in their overall revenue and DPU due to the reduced number of assets, I believe that the divestments were necessary to help FCT be prepared for any accretive opportunities that may come by.

FY2023 Results

Low Growth In Gross Revenue and NPI

| Year on Year Difference | FY2023 | FY2022 |

|---|---|---|

| Gross Revenue | S$369.723 million (+3.6%) | S$356.931 million |

| Net Property Income (NPI) | S$265.586 million (+2.7%) | S$258.597 million |

FCT performed as expected in FY2023 with low single digit growth, improving its Gross Revenue and NPI by 3.6% and 2.7% respectively. Considering the economy is still recovering post-pandemic, it is expected that FCT showed slow growth for the year.

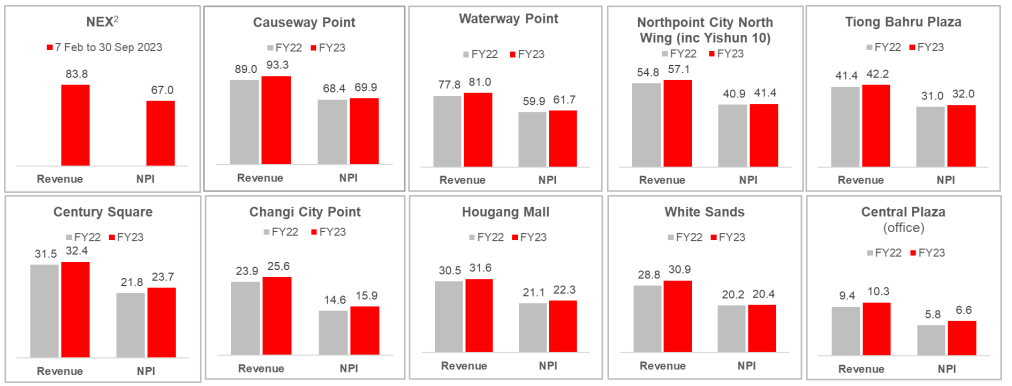

As we dive deeper into its portfolio, we can see that all its assets improved year over year in terms of Gross Revenue and NPI. Central Plaza, White Sands and Changi City Point were the biggest y-o-y growers in its portfolio mainly due to their smaller size which resulted in their percentage growth being larger in comparison.

Disrupted Distributable Income and DPU

| Year on Year Difference | FY2023 | FY2022 |

|---|---|---|

| Distributable Income | S$207.745 million (-0.2%) | S$208.19 million |

| Distribution Per Unit (DPU) | 12.15 cents (-0.6%) | 12.227 cents |

Despite the growth in Gross Revenue and NPI, FCT saw its Distributable Income and DPU distrupted by higher interest expenses in FY2023, which ultimately resulted in a year over year decrease of 0.2% and 0.6% respectively.

As we can see from FCT’s FY2023 income statement, the interest expense (marked as Finance costs), increased significantly by S$34.21 million or 73% year over year. As a result, it ate into the reurns of FCT drastically.

Balance Sheet Expected To Improve Post Divestment

| As at 30 September 2023 | As at 30 June 2023 | As at 30 September 2022 | |

|---|---|---|---|

| Aggregate Leverage | 39.3% (36.1%)* | 40.2% | 33.0% |

| Interest Coverage | 3.47x | 3.89x | 5.19x |

| Average Cost of Debt | 3.8% | 3.7% | 2.5% |

| Debt Hedged to Fixed Rate | 63% (73%)* | 63% | 71% |

* = Pro-forma effects post divestment

FCT’s balance sheet looks relatively weak as at 30th September 2023 but will improve significantly after its proposed divestments. As we can see from the table, the aggregate leverage is expected to improve to 36.1% and the percentage of debt hedged to fixed rate will improve to 73%. With the current high interest rate, it’s important for REITs to have a higher percentage of fixed rate debt if they currently have a managable or low cost of debt, so that their average cost of debt wont increase higher as rates increase. It also provides more stability as they wont be as impacted by interest rate changes.

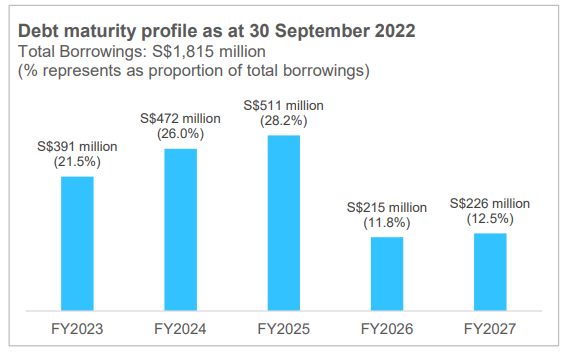

To explain further on why FCT’s average cost of debt increased drastically year over year despite having 71% of its debt hedged to fixed rates, we need to look into the debt maturity profile of FCT in 2022. As we can see, FCT had a total of S$391 million or 21.5% of its total debt expiring in FY2023. Coupled with the acquisition completed in February this year, for the remaining 50% stake in NEX, this put FCT is a very bad spot as they had to borrow more when rates were increasing at an accelerated rate. For additional context, in Q1 2023, the Singapore Overnight Rate Average (SORA) averaged 3.52% which means FCT had to borrow at rates higher than this. Moving into FY2024, FCT has already completed its debt refinancing for the year so there will not be any refinancing risk for FCT in FY2024.

Apart from FCT, I am keeping close tabs on all REITs that I have in my watchlist, keeping track on their respective balance sheets and valuation metrics. I also provide a quarterly update on these metrics to my Premium Subscription so that members can make an informed decision on which REITs are the safest and strongest.

Overview on Portfolio Stability

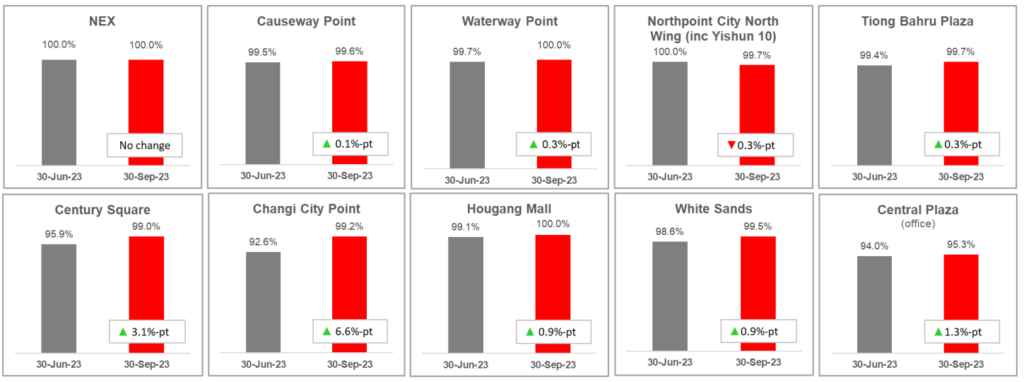

Last but not least, taking a deep dive into FCT’s overall portfolio, the overall Portfolio Occupancy has also improved by 2.2% to 99.7%, with the main contribution coming from Changi City Point (+6.6%), Century Square (+3.1%) and Central Plaza (+1.3%) which was slightly offset by Northpoint City North Wing (-0.3%). It’s also good o note that each of the retail malls has committed occupancy of at least 99%.

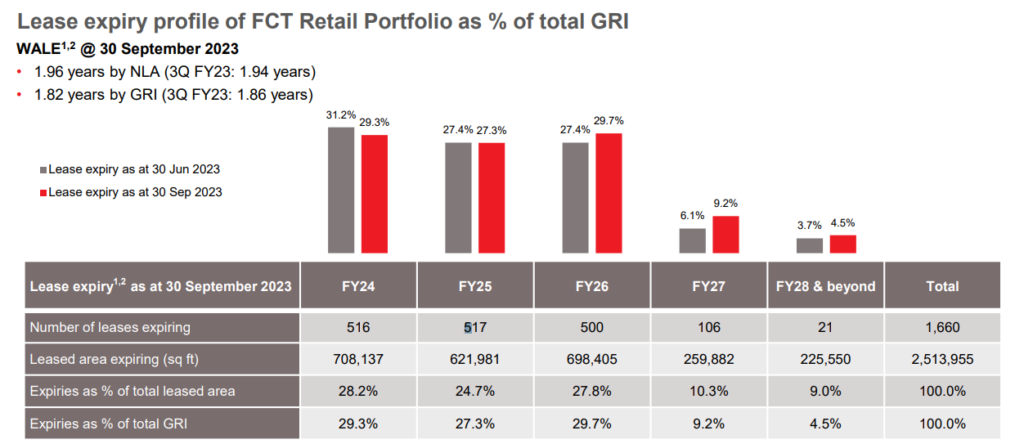

FCT’s overall portfolio WALE stands at 1.96 years in terms of NLA, a slight improvement from last quarter’s 1.94 years and, 1.82 years in terms of Gross Rental Income (GRI), a slight decrease from last quarter’s 1.86 years. It is good to note that leases expiring in FY2024 accounts for approximately 29.3% of GRI and 28.2% of NLA. Despite the sizable percentage expiring next year, I am confident in FCT’s management to not only renew but also acquire new tenants if current ones are churned out.

As for FCT’s portfolio rental reversion, we can see that when we compare incoming vs outgoing leases, FCT saw a +4.7% rental reversion in FY2023, as compared to +4.2% in FY2022. It’s good to see that all of FCT’s assets had a net increase in its average rental reversion with Changi City Point (+10.3%) and Northpoint City North Wing (+6.9%) being the main drivers that improved the rental reversion.

7-Year Performance

Revenue Growth

Note: Chart figures are in S$’000

As we can see, the overall 7-year trend for Frasers Centrepoint Trust is up. This is due to the fantastic management that has been aggressively growing the portfolio through meaningful acquisitions and investments over the years. The Gross Revenue has been shaky across the years but the NPI and Distributable Income has consistently gone up over the past 7 years with the exception of FY2023 where the Distributable Income saw a small drop.

There is a huge dip in FY2020 due to the covid-19 pandemic which heavily impacted the overall economy and retail sector. Taking aside the one-off black swan event, we can see that FCT has been doing well over the past few years and has performed well in FY2021 thanks to the acquisition of PGIM ARF.

Read Also: Frasers Centrepoint Trust Increased Their Stake In PGIM ARF! What Does This Mean?

DPU

Note: Chart figures are in S$ cents

Similarly, Frasers Centrepoint Trust has a very strong track record of consistently rewarding shareholders with increasing DPU over the past 7 years, excluding FY2020 and FY2023. With the fantastic acquisition of PGIM ARF this year, FCT has managed to bounce back from FY2020 lows to an even higher DPU now, beating the FY2019 (pre-covid) DPU.

NAV Growth

Note: Chart figures are in S$ dollars

The 7-year trend shows that Frasers Centerpoint Trust has managed to grow its NAV/share year on year consistently and at a relatively fast pace as well. FY2022 and FY2023 saw FCT’s NAV/share decrease minimally due to an increase in total units issued. This is very important because some REITs tend to see heavy dilution when doing acquisitions which results in shareholders indirectly losing value. As such, investors can use the NAV/share as well as DPU/share as indicators to determine if a REIT is truly bringing shareholders, increased value with acquisitions or are they only doing that “on paper”.

Divestment Analysis

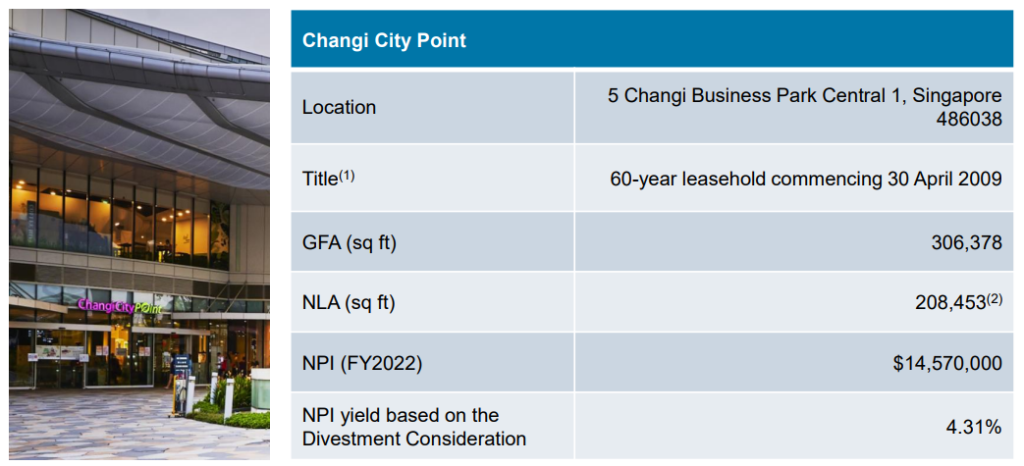

Changi City Point

As we can see from FCT’s FY2023 results, Changi City Point saw a huge improvement year over year, so why is FCT divesting it now? Changi City Point has seen a huge disruption in its footfall since the opening of Jewel which has become a very popular mall in Singapore. It is no doubt that Changi City Point will continue to see pressure in terms of footfall over time.

Additionally, the proposed divestment consideration of S$338 million is approximately ~4% above its current valuation of S$325 million. This will result in a net gain and capital gain of approximately S$10.9 million and S$20 million respectively. With the net proceeds, FCT can further strengthen its balance sheet and pay down its debt, further lowering its aggregate leverage as seen above.

Hektar REIT

As mentioned above, FCT holds a relatively big stake (~30.97% or 154,458,326 units) in Hektar REIT. The proposed divestment of Hektar REIT will see FCT sell 143,898,398 units which leaves FCT with 10,559,928 units or 2.12% of Hektar REIT’s total units outstanding. The divestment consideration is approximately MYR128.1 million (approximately S$37.4 million), based on the value of MYR0.89 (approximately S$0.26) for each of the Hektar REIT units sold. Similar to the Changi City Point divestment, this sale is also done above current valuation, as Hektar REIT’s closing price was MYR0.60 per unit as at time of divestment.

Although it isn’t mentioned if FCT made a net profit from this investment, we can actually backtrack to the time when they first acquired this stake in Hektar REIT and make an estimate from there. Despite not being able to find the exact average cost per unit, we know that FCT first acquired a 27% stake in Hektar REIT in May 2007. In this announcement, it is stated that FCT bought a total of 84.6 million units and paid MYR1.21 per unit which amounted to a total of MYR102.366 million.

Since then, FCT also increased their stake in Hektar REIT in June 2007 by acquiring an additional 13 million units bought at MYR1.33 per unit, amounting to MYR17.29 million. In 2012 due to a 4 to 1 rights issue, FCT acquired an additional 25,492,950 units at an issue price of MYR1.23 per rights unit which amounts to a total of MYR31.356 million. In 2017, Hektar REIT had another rights issue on the basis of 46 to 7. This resulted in FCT buying another 19 million units for MYR1.11 per rights unit, for a total of MYR21.1 million. This brings FCT’s total holdings in Hektar REIT to 143,898,398 units with a cost basis of MYR172.112 million or MYR1.196 per unit. From 2017 to 2023, FCT increased their total units by approximately 10.5 million but there isn’t any announcement on further units being acquired so we can assume the units were acquired through a Dividend Reinvestment Plan (DRIP).

From 2007 till date, Hektar REIT has distributed a total of approximately MYR1.4502 in dividends per unit. If we factor in the timing of distribution and the dividends distributed, FCT received an approximate total of MYR172 million in dividends. Based on the received dividends alone, FCT’s stake in Hektar REIT is already free of cost. This means that we can be sure FCT made a net profit on the sale, inclusive of fees and other expenses incurred through related transactions as well as forex differences.

All in all, similar to the Changi City Point divestment, the Hektar REIT divestment helps improve FCT’s overall balance sheet and opens up more opportunities should they present themselves such as new asset acquisitions.

Potential Growth Catalysts

Moving forward, investors should definitely consider if Frasers Centrepoint Trust has any potential growth catalysts left after the PGIM ARF portfolio acquisition. If not, this would mean that the REIT will start to stagnant and might not be as great of an investment as you think. Let’s cover a few potential growth catalysts that FCT might see in the near term as well as long term that can help grow the REIT.

Acquisitions From Sponsor Pipeline and 3rd Parties

As of 30 September 2023, aside from Frasers Centrepoint Trust’s main portfolio, they also own a 50% stake in Sapphire Star Trust (“SST”), a private trust that owns Waterway Point, a suburban shopping mall located in Punggol. The initial stake (40%) was increased in September 2022 and the transaction was completed in February 2023. FCT’s sponsor pipeline also includes Northpoint City South Wing, which is owned by Frasers Property and the TCC Group.

Among these potential acquisitions, the most likely will be Northpoint City South Wing from FCT’s sponsor pipeline. It is also likely for FCT to acquire a larger stake or even fully acquire SST, thus acquiring Waterway Point.

Asset Enhancement Initiatives

As usual, with all REITs, Asset Enhancement Initiatives (AEIs) are the most common and easiest way for the management to grow its portfolio without causing any dilution to shareholders. On the flip side, AEIs cannot really be anticipated or predicted because we don’t know which part of the portfolio and which specific asset can be further enhanced or improved.

Additionally, AEIs might sometimes require the asset to be left untenanted until it is completed. This could temporarily decrease the asset’s NPI and ultimately impact the portfolio’s performance. As such, investors should always look through the AEIs being done to understand the impacts that they will have on the overall REIT. In most cases, the AEIs tend to be accretive in one way or another, such as increasing the total NLA of the asset or improving the overall asset’s facilities to attract more tenants. The AEIs are usually found in the bottom section of every REIT’s business update or results presentation slides, in addition to the rationale for the AEI and expected completion date.

Currently FCT has an ongoing AEI for Tampines 1, which is expected to complete in December 2023.

Valuation

Of course, before we invest in any company, we should always do it at the right price and valuation. Based on Frasers Centrepoint Trust’s last closing price of S$2.04, its currently valued with a PB ratio of 0.90x and a annualized yield of 5.956%. When compared to FCT’s 5-year historical average PB ratio of 1.058x and dividend yield of 4.789%, FCT is also seen to be undervalued.

Valuation v. Peers

| Frasers Centerpoint Trust's Peers | PB Ratio | Annualized Dividend Yield |

|---|---|---|

| CapitaLand Integrated Commercial Trust ($1.74) | 0.84x | 6.092% |

| Lendlease REIT ($0.495) | 0.63x | 9.495% |

| Paragon REIT ($0.80) | 0.89x | 6.050% |

| Starhill Global REIT ($0.45) | 0.63x | 8.444% |

As compared to its peers like CapitaLand Integrated Commercial Trust, Lendlease REIT, Paragon REIT (used to be known as SPH REIT), and Starhill Global REIT, we can see that Frasers Centrepoint Trust is actually trading at a slight premium as compared to its peers, with Paragon REIT trading closest to FCT in terms of valuation. When comparing the annualized dividend yield, we can see that FCT is above the average amongst its peers.

Final Thoughts

Frasers Centrepoint Trust has definitely been one of the key REITs that I have been monitoring for a long time now. Since FY2020 after I predicted the PGIM ARF portfolio acquisition, I accumulated FCT in 2 tranches, the first at 2.59 and the second during the Preferential Offering (PO) at 2.34. Since then, I have sold my holdings earlier this year due to my forecast of a looming recession soon to hit the economy.

Despite this, my long-term price target is way beyond $3 as per most analysts’ price target and that there is a huge upside for FCT. The enhanced portfolio combined with the recovery of the economy back to pre-covid levels will definitely bring FCT to greater heights, way beyond its past highs.

Pingback: My Top 5 Exciting REITs To Watch in 2024